Anyone who’s seen a zombie horror flick knows you can’t trust the government in times of an undead apocalypse. They’re just as likely to shoot you as help you when it comes to quarantining the brain-eating zombies who were once your friends, family and neighbors.

In the housing market, an outbreak has already struck—a foreclosure crisis that has spread like a virus across the country. Kicking folks out of their homes and filling the market with zombie homes that infect neighborhoods with deflated values increases the likelihood of more foreclosures, which gives rise to an undead community—even a zombie economy, lurching slowly away from recovery.

And some Utahns in search of help have found the government just as likely to push them toward foreclosure as save them from it.

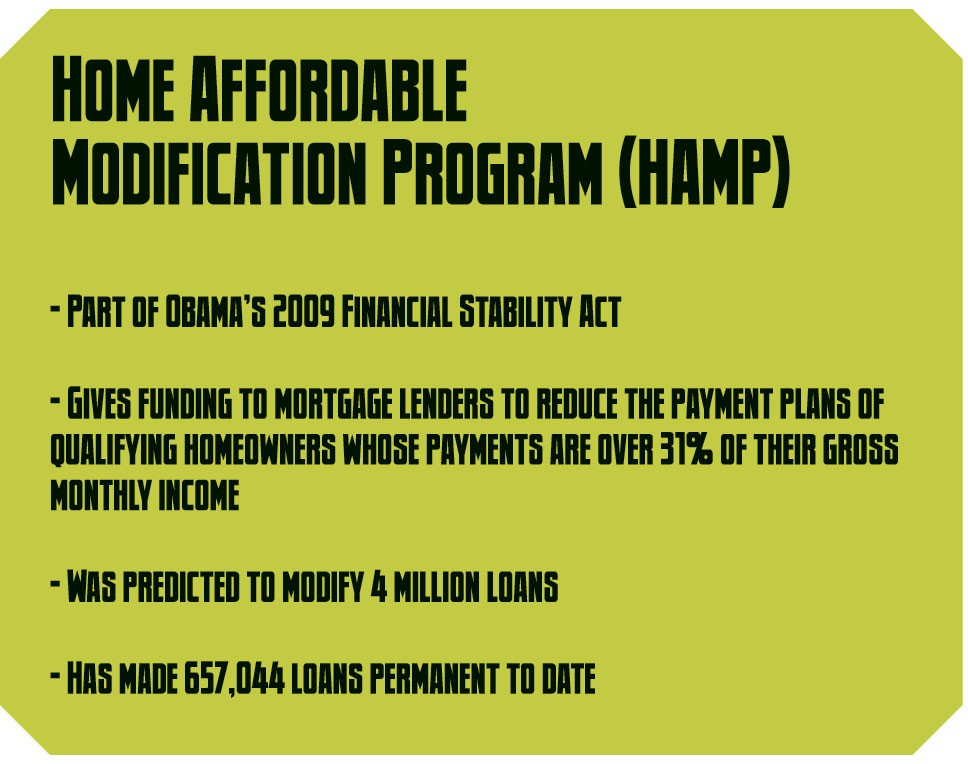

Terrie Combs thought it couldn’t hurt to ask when she inquired about a loan-modification program offered through her mortgage holder, Bank of America. The program was subsidized by the Treasury Department through President Barack Obama’s Home Affordable

Modification Program (HAMP), commonly referred to as the Making Homes Affordable Program.

Combs waited months for her application to be approved, unaware that Bank of America’s foreclosure arm, ReconTrust, was at the same time moving forward to take her home. Combs learned that she had not been approved for the modification only after her home had been sold and she was served notice to vacate.

Combs, who runs a small pizza chain with her husband, is still shocked at how the HAMP program not only didn’t make her home affordable, but also allowed Bank of America to string her along with promises of salvation while simultaneously swooping in with foreclosure. In frantic phone calls that placed her with call centers as far-flung as Costa Rica, Combs says she got different responses nearly every time and no answers, as loan-modification representatives acted as if they had no control over the foreclosure department’s actions.

“It’s like Bank of America doesn’t even know who ReconTrust is,” Combs says, “and ReconTrust is Bank of America!”

Combs is not alone. Marco Fields, a housing advocate with TEEMS Utah, a nonprofit organization that helps homeowners fight wrongful foreclosure, says she is flooded with daily calls about similar stories involving numerous national banks. She sees Utah’s foreclosure crisis as being exacerbated by the HAMP program, whose major flaws have been exploited and botched by loan servicers in a way that makes the problem worse.

“People think the foreclosures are going down—they’re not. What is happening is there are so many people defaulting that the banks can’t keep up with filing notices of default,” she says, adding that there is about a three-month backlog of foreclosures that have not yet been publicly posted.

“That is terrifying,” Fields says. “By the end of the year, we’re going to see more than 50,000 foreclosures,” compared to the 32,000 posted in 2010. It’s the kind of problem Fields says will drag Utah’s economy down for years or even decades if action isn’t taken now.

“It is a fundamental community and state crisis,” she says.

But it’s hard to point a finger at one culprit for causing the foreclosure outbreak. While many homeowners would like to point at least a middle finger at banks and loan servicers like Bank of America, which is currently the subject of numerous lawsuits around the country, Rick Simon, a spokesman for Bank of America, points out that the HAMP program changed its guidelines regularly and had inconsistencies that added confusion and delays to the modification process. Simon says it was also hard to prepare for the flood of applicants seeking modification.

“There was a traditional way these things worked, and we’ve turned that on its end completely over the past two years,” Simon says.

Advocates like Fields understand there aren’t easy-to-pinpoint culprits, but she and others say no matter the cause, all of Utah’s state and federal leaders will be at fault if they don’t act now to help protect Utah homeowners. She points out that in July, funding ran out for local nonprofits to continue to employ federally trained foreclosure-prevention counselors. A year prior, the state’s 20 Housing and Urban Development-certified counselors helped stave off 1,292 foreclosures.

“We have a third of the HUD counselors we had from this time last year,” Fields says. “We went down from 20 to six, and pretty soon we’re going to be down to two. All the money’s gone.”

HAMPered

Fields, the founder of homeowner advocacy organization TEEMS Utah, says the HAMP program was launched in 2009 with poor guidelines and no penalties for banks that didn’t follow the program’s guidelines.

Fields says that since 2009, the program has worked better at getting clearer guidelines for everyone involved, from homeowners to the loan servicers who hold the mortgages and investors whose bottom line is tied up in pools of loans. But even with all the refinement that’s happened, it’s still a confusing and distressing process for homeowners.

“The problem is that the banks’ and investors’ guidelines change every four to six weeks,” Fields says. “And the poor little homeowner who is trying to get some kind of relief gets stuck in this cycle and goes around and around.”

Among the problems that have beset the program is that homeowners who seek a HAMP loan modification through their loan servicer undertake a trial modification that lets the homeowner make reduced mortgage payments while his or her financial information is vetted by the bank or loan holder. But while the application is being processed, the foreclosure process is not stopped. So, if the application process drags on too long, foreclosure will hit well before a bank can even determine whether the applicant is approved for the modification. While HAMP guidelines say a bank can’t foreclose on a home that is under consideration for loan modification, Fields says banks often don’t tell an applicant they’re not approved until their home is already on the auction block.

Contrary to the law, banks and servicers sometimes won’t even tell homeowners why the modification was denied.

At the beginning of August 2010, Combs faced two perilous deadlines. Bank of America’s loan agent told her that despite more than four months of asking for and receiving paperwork from her, they needed more information and they needed it by Aug. 18. Meanwhile, Bank of America’s foreclosure subsidiary, ReconTrust, gave her a warning of accelerated foreclosure saying that she owed $2,800 in missing payments, and if they didn’t receive it by Sept. 5, her home was to be sold on the courthouse steps.

Those “missing” payments, Combs says, were the funds that were reduced from her payment as part of her trial modification, and she says she had been told not to make those payments.

When Combs called on Aug. 18 to find out if they had received the payment, she was told that they had sold her house already, on Aug. 12. She says she was told that they did not have to tell her that she was not approved for the program. When she sought to stop the sale, she was given the cold shoulder, she says.

“I had equity in my house, so it was a really good find for that investor,” Combs says. “Bank of America came back and said, ‘According to state laws and our investor guidelines, we can’t rescind your sale; you had plenty of time to do your paperwork—goodbye.’ ”

Trials and Tribulations

The hair-pulling frustration of the HAMP application process is part of why HAMP often hurts homeowners instead of helping them. If paperwork is lost in the shuffle while homeowners are paying less on their mortgage—as they’re told to do—then those “missing” payments will help accelerate the foreclosure process.

With many factors to consider, it’s hard to assess the effectiveness of banks or servicers when it comes to turning trial modifications into permanent ones. But on the state level, at least, some servicers have performed better than others.

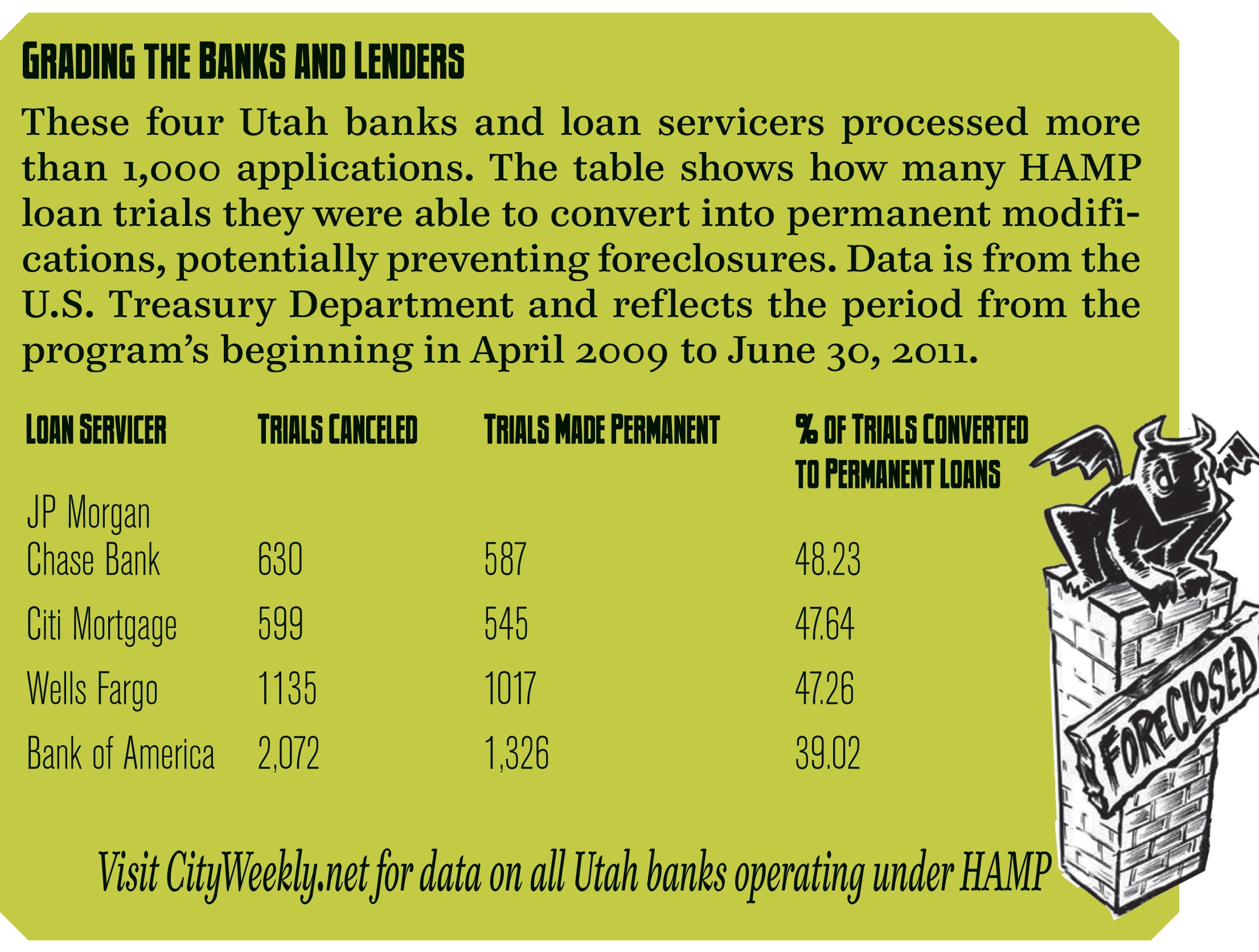

According to records obtained from the Treasury Department through a Freedom of Information request, 68 loan servicers in Utah have processed 13,290 HAMP trials, from the program’s start through June 30, 2011. Statewide servicers have been able to convert 64 percent of those trials into permanent modifications.

The poorest performer for large servicers in Utah was Bank of America, which converted only 1,326 of its 3,398 trials into permanent loan modifications—or 39 percent of applicants (see table below).

“There was a lot of pressure on larger servicers to get the program up and running,” says Bank of America spokesman Simon. While Simon could not speak to the conversion performance of his bank in Utah, he says that, in general, Bank of America and other large servicers struggled with the Treasury Department’s often-changing guidelines.

Ironically, while a large factor behind the 2008 housing meltdown was the fact that borrowers could receive large loans simply by stating their income without documentation, Simon says that when HAMP was launched in 2009, it also allowed homeowners to simply state their incomes when applying instead of providing documentation. That process, he says, slowed the process down by forcing servicers to underwrite loans twice, giving a trial based on stated financials and then following through with a separate underwriting process once they received actual financial documents. Since that rule was changed to require documents up front starting June 1, 2010, he says Bank of America has averaged a trial period of 3.3 months, slightly below servicers’ national average of 3.5 months.

He also says Bank of America is planning to move to a system where each loan modification will be handled by one case manager who will hold all the documentation for a homeowner, preventing crucial documentation from getting lost in the shuffle.

“It took some time to get out of that traditional mode that couldn’t deal with the volume [of applications] we’re handling today,” Simon says.

Simon could not speak to ongoing legal battles such as the negotiations Bank of America is currently involved in with the state of Utah about homeowners being foreclosed on illegally, but hopes those problems are behind his organization.

“We haven’t been perfect,” he says. Still, he argues that HAMP—when it works—is the best option for many homeowners looking to keep a roof over their head.

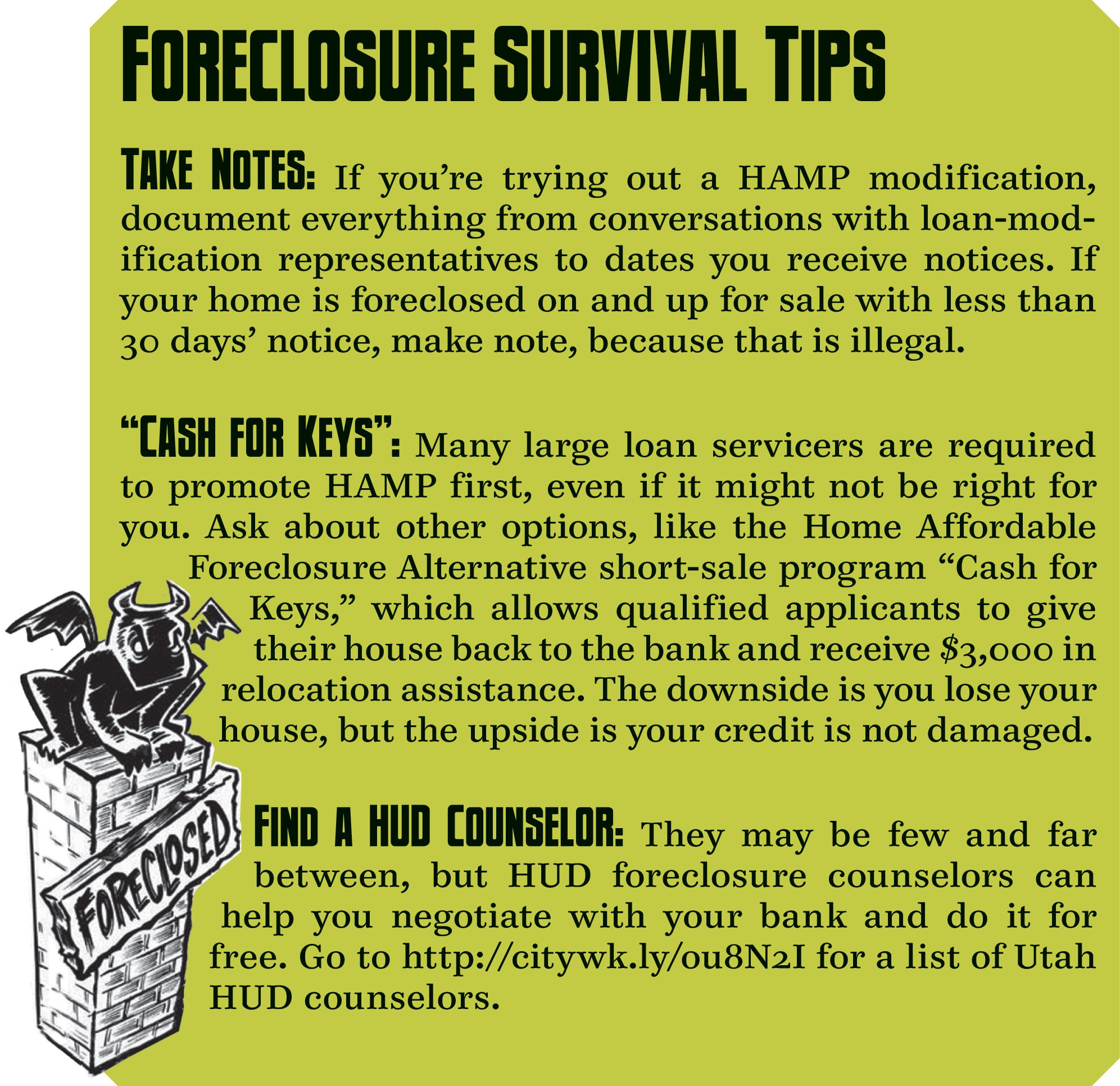

But for advocates like Fields, HAMP is a “Hail Mary” that, even in its latest manifestation, is full of flaws. Even if it works, she says it can surprise homeowners with unexpected debts and fees that sneak onto their loan (see below for tips on dealing with foreclosure).

Collision Course

The three letters a loan-modification seeker probably doesn’t know about, but should worry the most about, are NPV, which stands for Net Present Value. In HAMP guidelines, NPV represents a tipping point at which foreclosure is allowed if it looks like the investor entitled to a piece of a homeowner’s mortgage—because they invested in a pool of loans—will come out better if the home is foreclosed on, rather than modified.

The problem is that a servicer needs to lower applicants’ payments to 31 percent of their monthly income. To do this, banks will sometimes manipulate the modification in ways that drop the NPV value and speed up the foreclosure process. Banks and servicers, for example, will add forbearances to a loan—payments that are deferred but have to be paid at the end of a loan or when the home is sold. Fields says those balloon payments are many times added without a homeowner’s knowledge, and can hurt their credit years down the road.

Torrie Valdez knows from experience how the HAMP program helped put her home on the brink of foreclosure—she waited 18 months through three applications to hear if her modification would be made permanent.

Valdez’s financial troubles, like those of many others, began in 2008, when a sudden divorce also left the West Jordan mother with the challenge of trying to keep her home on a limited income. She estimates that she was behind as much as $5,000 in payments when she began her first HAMP trial. Now, after struggling through an 18-month paper shuffle with Bank of America and hiring an attorney to fight her wrongful foreclosure, Valdez says her debt is more than $60,000.

“I would have rather been foreclosed on,” in 2009, Valdez says with exasperation. “It’s just been a ride.”

When she was enrolled in the trial, she was told, as all applicants are, that she would be making reduced payments for three months. Those three months became a year and a half.

“Then, all of a sudden, they stopped taking my payments,” Valdez says. With foreclosure notices hitting Valdez nonstop, she says she was in a panic.

“I was begging them to accept my payments,” she says.

Prior to that, however, Valdez says loan-modification representatives at the bank would tell her she needed different requirements every time she talked to them; the only consistent message they relayed was that everything was fine and that a permanent modification was just around the corner. She even received numerous letters assuring her that she was qualified for a permanent modification.

“Here’s the bottom line: I don’t want anything for free. I owe the money, and I should pay the money—just allow me to do that,” Valdez says. “[But] don’t let me pay for just shy of two years and let me think I’m OK, and then try to take my house. That’s a crock of you-know-what.”

While both Valdez and Combs were able through attorneys to keep their homes, it still cost them.

“To sue these national banks is very costly,” Fields says. “I believe banks count on that. They’re preying on the segment of Americans that can least afford to defend themselves.”

Valdez got a restraining order to keep Bank of America from taking her home, but it still has set her back. Before she was able to get an attorney and counseling services from Fields, Valdez had been supporting herself by running a home day-care business. She had to shut it down in September 2010 when foreclosure seemed imminent.

“It’s pretty hard to run a business from your home if you don’t have a home,” Valdez says.

Zombie Economics

The zombie-home apocalypse that has ravaged America since the housing crisis of 2008 has spread wildly, but also surreptitiously. These undead homes have appeared in neighborhoods as disheveled, worn-down semblances of the happy homes they once were. Instead of white picket fences and manicured yards, these zombies mar neighborhoods with broken windows and unkempt lawns—and they aren’t just eyesores. According to statistics from the 2008 Joint Economic Committee of Congress, a single foreclosed home represents a $77,935 loss to the local economy, when counting the cost to lenders, legal bills, moving expenses and lost equity for evicted homeowners, lost taxes to local city governments and lost home values for neighbors to a zombie home.

“It’s like a flesh-eating bacteria—pretty soon it just erodes everything,” Fields says.

Afton January, a foreclosure specialist with nonprofit Utah Housing Coalition, has been watching Utah’s foreclosure epidemic since the 2008 meltdown. She says that the $77,935 doesn’t include money homeowners put into the economy.

“People going through foreclosure don’t have money to spend on local restaurants, movie theaters and retail businesses,” January says. She says it also doesn’t factor in the increased pressure put on the rental market as displaced homeowners find themselves moving into cheaper apartments and condos.

“My rent has gone up, and part of the reason it’s gone up is more and more people are looking for rentals,” January says. “It affects me even though I’ve never owned a home.”

January feels the foreclosure fight needs more HUD counselors on the front lines.

In 2009, she was tasked with distributing $1.8 million in stimulus funds set aside by former Utah Gov. Jon Huntsman to fund Housing and Urban Development training and certification for members of local housing nonprofits to become foreclosure counselors. As of July 31, those funds have run out. But in that time, local counselors helped prevent 1,292 foreclosures in the state—providing enormous savings for the state economy, January says.

“This really affects everybody,” January says. Using statistics provided by the 2008 Joint Economic Committee of Congress, January calculated national estimates of the ripple effect of a foreclosure and applied them to Utah to demonstrate that preventing 1,292 home foreclosures could have saved Utah as much as $100,692,020.

Fighting the Apocalypse

In the 2011 legislative session, Sen. Curtis Bramble, R-Provo, passed Senate Bill 261, a bill he says was “more than a shot across the bow” for banks performing illegal foreclosures in the state. The bill makes specific in Utah law that foreclosures need to be executed by agents who have the physical deed to the house. The foreclosing entity likewise cannot fail to inform the homeowner that despite them being on a reduced payment plan, it doesn’t stop them from foreclosing. Penalties from the bill include having greedy banks and servicers pay plaintiffs’ attorney fees, as well as a $2,000 fine or special damages, whichever is higher.

Bramble says this law gave the Utah Attorney General’s Office the “teeth” to go after reckless actors like Bank of America, who are currently negotiating a settlement.

In tackling the issue, the Legislature is put in a precarious position, Bramble says.

“On the one hand, preserving property rights is critical; on the other, protecting the borrower is also critical, and at the same time, preserving the rights of the person loaning the money is critical,” Bramble says.

That’s three prongs of the issue, but still doesn’t take into account the economic and political reality that establishing programs to help save Utahns’ homes from foreclosure and zombification may require expanding government—a move not often welcomed by Utah’s conservative, small-government-minded Legislature.

Bramble says he and his colleagues on the Hill are ready to take the issue further in the next session and are even open to the idea of finding a way to provide more funding for nonprofit counselors, though he prefers the idea of creating a state foreclosure-arbitration office.

“I’d have it be a state ombudsman, rather than just going to private sector arbitration,” Bramble says. “I think it would be self-funding; we could do it through lender-licensing fees.”

Such an independent office could work much in the same way a Utahn goes through divorce mediation as a means of savings costs in the long run. With a foreclosure-arbitration office, an independent state employee could be a referee between bankers and homeowners, both to keep homeowners from abusing the process and protect homeowners from being bullied by big banks.

Bramble says so far nothing is off the table. Like advocates Fields and January, he believes Utah has yet to feel the full brunt of the foreclosure crisis.

“I don’t know that the dust has settled in that arena yet,” Bramble says. “I would say now we may not yet be aware of the [crisis’] magnitude.”

For Fields, any settlement the state brokers with Bank of America could go a long way to funding arbitration programs, HUD counselors and even a legal fund for people fighting wrongful foreclosures.

“Unfortunately, we’re struggling with resources in this state,” Fields says. “Other states have aggressively funded outreach programs and foreclosure-mitigation programs. Twenty-seven states have mediation programs that are working very well.”

Life, Zombified

Zombie homes are here, and they’re slobbering at the chance to gnaw away at the values of the homes around them and, in turn, infect an economy that affects everyone—even those who don’t own homes. With advocates warning that the HAMP program can do more harm than good, and with the state still locked in legal negotiations with Bank of America, homeowners are still looking for help and will continue taking it wherever they can get it.

For Cody Livingston, help came too late.

Livingston, now 34, was newly engaged two years ago when he started building his home. It was a night-and-day labor of love to finish the home in time to have it ready for his wedding. But, in summer 2010, Livingston was evicted from the home he had built with his own hands. Like many others, Livingston’s saw his credit take a pummeling because of the foreclosure process; also like many others, he was strung along for 11 months by Bank of America’s loan-modification customer-service representatives who, he says, reassured him that his reduced payments wouldn’t count against him since he was only moments away from getting his permanent modification.

“I was never late, never even close to missing a payment until [Bank of America] contacted my wife to ‘help us,’ ” Livingston says. “All they did was help me lose my house.”

Now fighting to repair his credit and get his finances out of the red, Livingston has been forced to lease a home for his family, in the same neighborhood as the home he had built.

“I drive by my house every day,” Livingston says. “My old house, I should say.”

More by Eric S. Peterson

-

The Secret Sauce

How Utah lawmakers disclose—or don't disclose—conflicts of interest.

- Feb 14, 2024

-

Police departments in Salt Lake County spent almost $20 million on civil rights complaints in the past decade

The Co$t of Mi$conduct

- Oct 18, 2023

-

Women decry harassment and toxic culture at St. George auto dealership

Men at Work

- Oct 11, 2023

- More »

Latest in Cover Story

Readers also liked…

-

Forget the family pedigree—Robert F. Kennedy Jr should not be the next president of the United States

Trojan Horse

- Jun 21, 2023

-

Women decry harassment and toxic culture at St. George auto dealership

Men at Work

- Oct 11, 2023

{kind=link}